Dear Investor,

Are you also looking forward to finally enjoying the first rays of sunshine and being able to go back to your favorite beer garden? Winter has lasted long enough, and spring is cautiously extending its feelers. The clocks have already been changed, and April 23rd is German Beer Day.

Germany used to be considered the number one beer-drinking country. Now, in a European comparison, Germany ranks only third in beer consumption, but is still the largest beer producer in Europe, ahead of the UK.

In international comparison, the largest German brewery, Radeberger (with brands such as Jever, Clausthaler or Schlösser Alt), only ranks 22nd.

With the arrival of spring, the question arises whether the large, publicly traded breweries can benefit from the improving weather. To investigate this, we examined three major breweries and analyzed the seasonal effects.

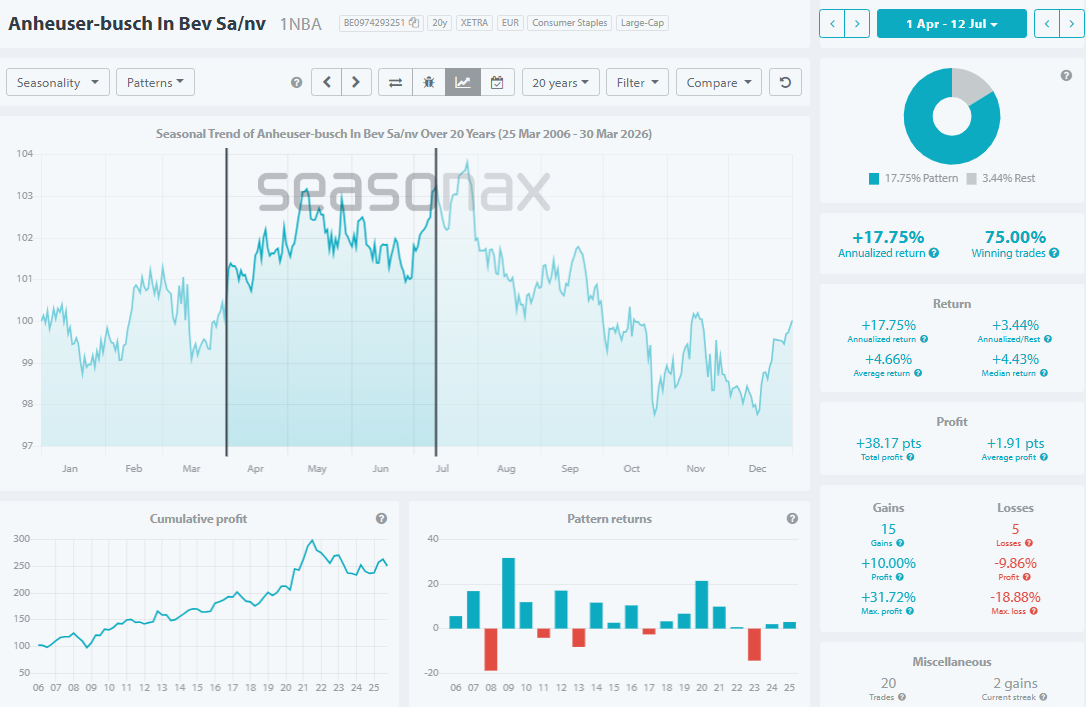

Anheuser-Bush InBev is the dominant player among the large publicly traded breweries

This world’s largest brewing group emerged from a merger of the well-known Budweiser brand from the USA with the Belgian Interbrew (which had previously merged with the Brazilian AmBev from Brazil).

The best-known brands are Budweiser, Beck’s, Corona Extra, Leffe (abbey beer from Belgium) or Stella Artois.

The seasonal chart shows that the beginning of the beer garden season is likely to lead to an increase in revenue.

In an impressive 15 of the last 20 years, Anheuser-Krauts has seen a pleasing average increase of 10% between April 1st and the summer. Even though the five years with losses also saw a decline of almost 10%, these statistics show that spring is clearly a good time for the largest brewery.

Source: Seasonax | View pattern

Although it may seem at first glance that the beer-drinking season ends in the height of summer, the period up to mid-December is almost balanced. While a statistical advantage can be drawn with a ratio of 9 to 11 positive to negative years, a sustained decline is not expected during this time.

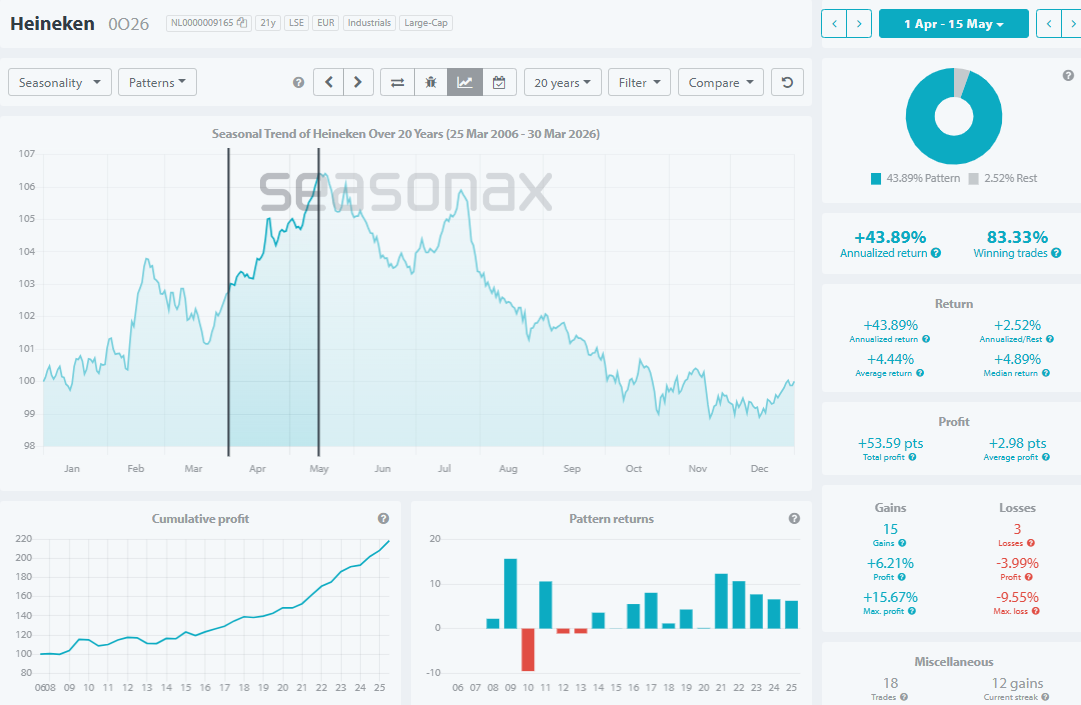

The Dutch company Heineken ranks second and is hardly behind the industry leader

With its core brand Heineken, the Dutch brewer is known and loved worldwide. Other brands include Affligen (abbey beer) and Amstel (the big Belgian).

Unlike Anheuser-Bogen, Heineken’s spring upswing only lasts until mid-May, but boasts impressive statistics over this period, with a return of 15 years compared to 3 years for Anheuser-Bogen. Even though the average yield is only around 6%, this is quite respectable for such a short period.

Source: Seasonax | View pattern

From the end of July to the end of October, beer drinkers seem to turn their backs on Heineken as well. This downward trend is particularly pronounced, with 14 negative periods in the last 19 years. Furthermore, the last 10 years have all been negative. During this period, an average return of almost 10% could be achieved with a short position.

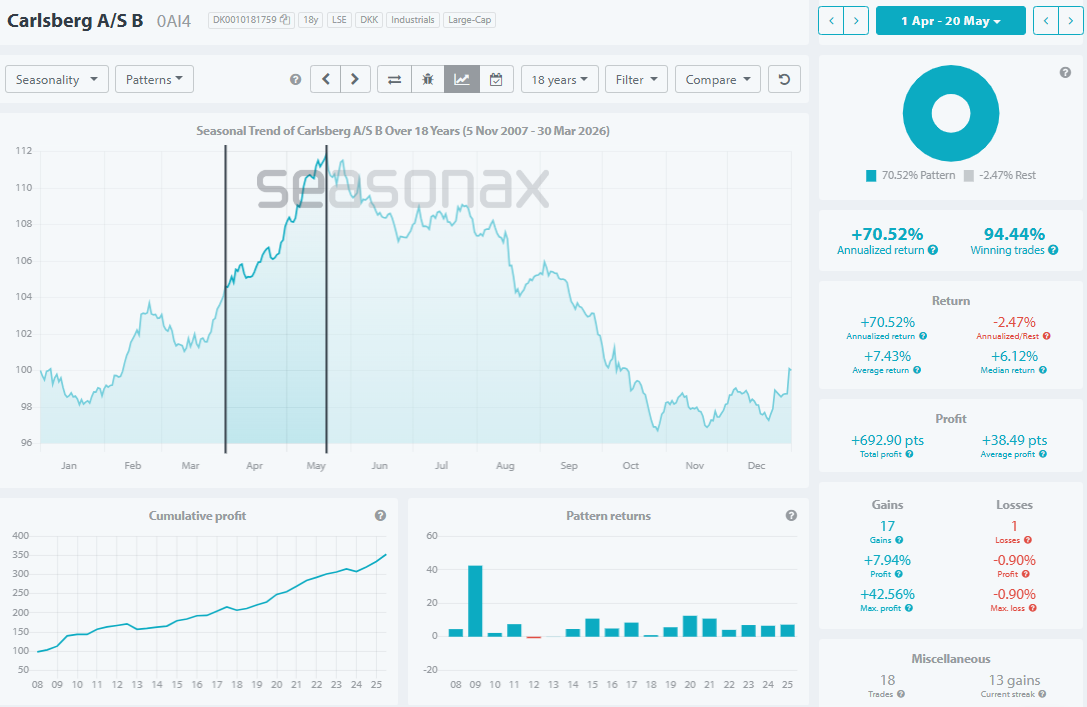

Danish company Carlsberg is the leader

Although Denmark doesn’t have the highest alcohol prices in Scandinavia, they are still significantly above the European average and far above the German average. Nevertheless, the Danish Carlsberg Group, with brands like Tuborg, Holsten, and Kronenburg (France), ranks among the largest brewers, right behind Heineken and Anheuser.

Source: Seasonax | View pattern

The period already described for the other two brewers is particularly compelling in the case of Carlsberg. With a return of 17 to one year, the yield in recent years was almost 100%. For the period from the end of March to the end of May, an average return of nearly 8% is a remarkable performance. However, this upward trend also came to an end on May 20th, resulting in a negative statistic of 6 to 12, with around 20% in the twelve negative years.

Why do breweries only raise their prices until midsummer?

This unusual behavior is apparently due to the brewers’ typically peak sales up to July, which is then reflected in their profit expectations. Experience shows that the weather becomes more unsettled in the second half of the year (even though autumn still has some warm days), which weakens sales prospects. Therefore, a strategy could be employed that combines long positions in the first half of the year with short positions in the second.

The classic charts reflect high volatility, which is also evident in the Seasonax charts. Therefore, while these beer stocks are not suitable for investment, the Seasonax charts are an excellent tool for exploiting these fluctuations.

Conclusion: Beer will always be drunk, even if sales figures in Germany are declining.

Beer is considered a staple food, and this is unlikely to change in the foreseeable future. The spring periods of the major breweries are so noticeable and pronounced that they can be effectively used for trade.

Earn your next beer garden visit with your friends with the opportunities that Seasonax offers you, not just with brewery shares.

Take advantage of the benefits and use Seasonax for your professional handling of seasonal trends!

Best regards,

Christoph Geyer, CFTe

Winner of the Stock Analyst Award for Technical Analysis