Dear Investor,

Copper is often referred to as “Dr Copper” because of its reputation for signaling the health of the global economy. However, despite the powerful long-term demand story surrounding electrification, AI infrastructure, and grid expansion, copper is now entering one of its weaker seasonal periods of the year. This may create an opportunity for buying at lower prices for the savvy investor.

The chart below shows that over the last 15 years, copper has produced an average return of –4.11% from 27 May to 7 August, with a win rate of just 26.67% and an annualized return of –19.28%. Pattern returns also show repeated summer weakness, with downside pressure emerging consistently during this window. There have also been some notable recent falls during this seasonally weak period. In 2021 copper fell 11.81%, in 2022 it fell a substantial 25.18%, and in 2024 there was another significant drop of 18.72%. So, seasonally this is a weak period with recent drops into double digits.

From a tactical point of view this is really interesting. There are some potential reasons for particular seasonal pressure this summer. However, while the short-term seasonal outlook may appear soft, the broader structural bull case for copper remains firmly remains. Let’s now explore reasons for copper weakness this summer.

Why Copper May Face Seasonal Pressure into Summer

One important driver for this year for recurring seasonal weakness may be current demand sensitivity for copper at elevated price levels, particularly from China, the world’s largest metals consumer.

Recent reports suggest that copper prices near record highs have begun to deter near-term demand from Chinese fabricators, with orders weakening in May as buyers resist higher prices. This comes after COMEX copper surged to an all-time high of $6.7160 per pound in May, driven by supply concerns and expectations of stronger Chinese demand.

At the same time, speculative positioning has become increasingly crowded. According to recent US government CFTC data, money managers increased bullish copper bets by 16% to 73,523 contracts in the week ending May 12, the highest level since December. Elevated positioning like this can often leave markets vulnerable to temporary profit-taking and sharper pullbacks during seasonally weak windows.

In summary the near-term seasonal weakness may have some more specific drivers, namely:

- Stretched bullish positioning

- Demand slowdown at elevated prices

- Seasonal summer softness

- & general reduced industrial activity during mid-year months

Together, these factors could help explain why copper may struggle during this coming seasonally weak period.

But the Bigger Picture for Copper Remains Bullish

Despite the weaker seasonal backdrop, the long-term investment case for copper continues to strengthen.

Copper sits at the center of several major global trends:

- AI data center expansion

- Electricity grid upgrades

- Electric vehicles

- Renewable energy infrastructure

- Defense spending increases

AI infrastructure alone is expected to require enormous amounts of copper as hyperscale data centers demand vast increases in electricity generation, transmission capacity, and cooling systems.

At the same time, supply growth remains constrained. Major mining projects face:

- Long development timelines (sometimes 10 years plus)

- Political permitting risks

- Declining ore grades

- Rising capital costs

This creates the possibility that future demand growth could outpace new supply for years to come.

A Tactical Dip Inside a Structural Bull Market?

This creates an interesting setup for investors.

While seasonality suggests copper may struggle into the summer months, any pullback could potentially offer longer-term investors an opportunity to build exposure within a broader structural uptrend. The cumulative profit curve on the Seasonax chart clearly reflects this seasonal softness.

The cumulative profit curve on the Seasonax chart clearly reflects this seasonal softness.

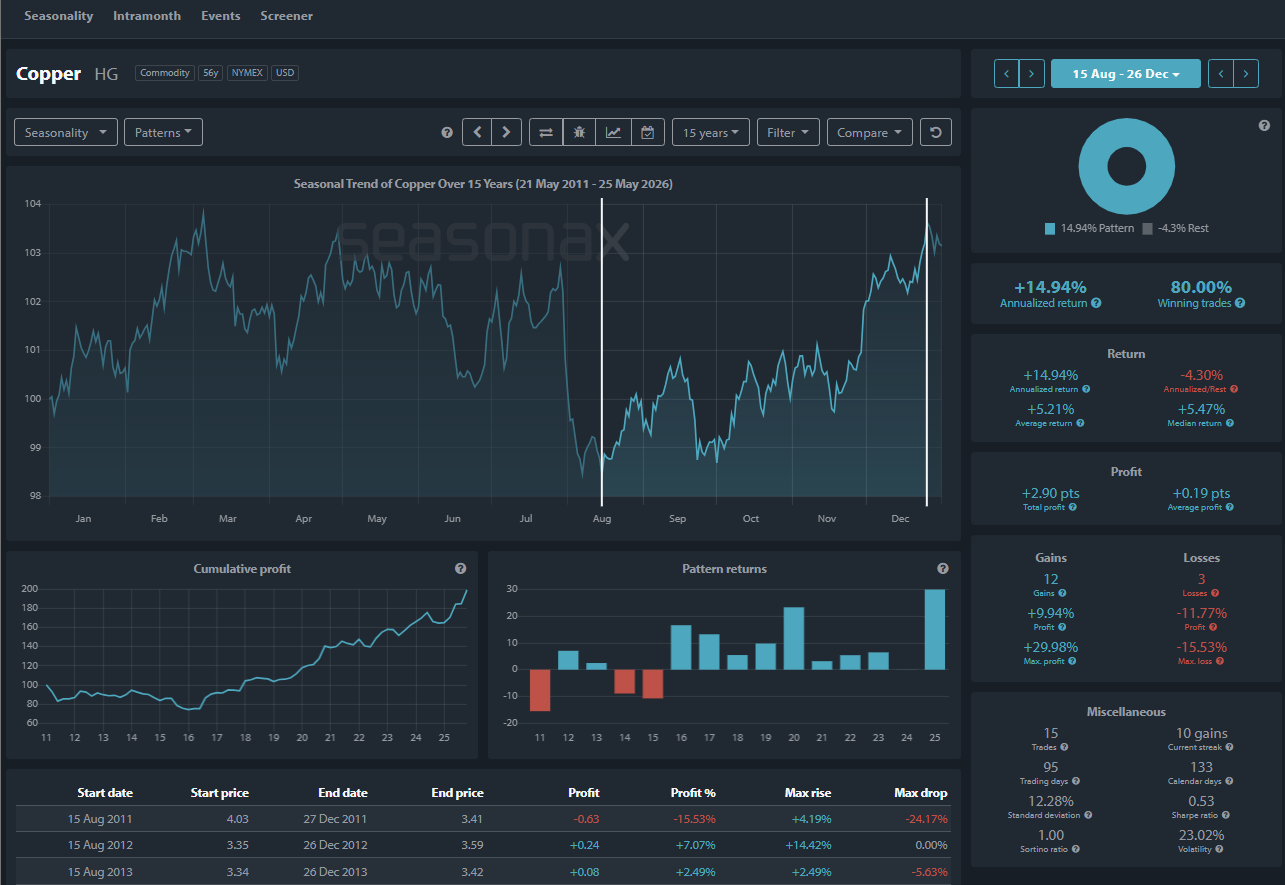

However, Seasonax also highlights below how sharp reversals can emerge once summer weakness fades later in the year. The chart below shows that after copper’s weak seasonal period from late May into early August, the market historically transitions into a much stronger phase from 15 August to 26 December, delivering an average return of +5.21% with a strong 80% win rate over the last 15 years.

The cumulative profit curve below again highlights how copper’s seasonal weakness phases into a sustained recovery into year-end, suggesting that summer softness has historically created opportunities for longer-term positioning.

Trade Risks and Opportunities

Copper’s weak summer seasonal window should not be ignored. In the light of speculative positioning elevated and Chinese demand showing signs of cooling at high prices, further near-term volatility remains possible.

Key risks include:

- Further deterioration in Chinese industrial demand

- Profit-taking from heavily long speculative positions

- Slower global growth expectations

- A stronger US dollar weighing on commodity prices

However, the longer-term structural drivers behind copper demand remain extremely powerful. Any meaningful seasonal pullback may therefore attract buyers looking to position for:

- AI infrastructure expansion

- Electrification trends

- Tightening long-term copper supply

For longer-term investors, seasonal weakness may ultimately prove to be a perfect opportunity for entering a broader bull trend.

Use Seasonax for your professional handling of market-moving seasonal trends!

Don’t just trade it – Seasonax it.

Giles Coghlan, CMT

Macro Strategist Seasonax